Everything to know about Electronic Clearing Service(ECS) - BANKING TERMS FOR EXAMS

- BANKING TERMS FOR EXAMS")

What is Electronic Clearing Service?

ECS - Electronic Clearing Service is an electronic mode of payment for transactions that can be used for making bulk payments or receipts. This facility is used by institutions for making bulk payment of amounts towards the distribution of dividend, interest, salary, pension, etc., or for bulk collection of amounts towards telephone/electricity /water dues, cess/tax collections, loan installment repayments, periodic investments in mutual funds, insurance premium etc.History of ECS

Image-based Clearing System (ICS) or Cheque Truncation System (CTS) is a project started by the Reserve Bank of India (RBI) in 2010, to speed up the processing of cheques in banks. CTS is based on an image-based clearing system where Magnetic Ink Character Recognition (MICR) data and cheque images are transmitted by the collecting bank to the drawee bank. The CTS stops the flow of physical cheques between the collecting branch and the drawee branch. At some point en route to the drawee branch an image of the cheque and the MICR data are captured and transmitted to the drawee branch, this has eliminated the need to move physical instruments between branches, thereby, reducing the time taken to process cheques and the costs associated with physically moving instruments between branches. The Cheque Truncation System (CTS) was first implemented by the Reserve Bank of India in New Delhi on February 1st, 2008 with 10 pilot banks with a deadline of 30th April 2008 for all banks. CTS was launched in Chennai on 24th September 2011. After the migration from MICR to CTS, the MICR system was discontinued in NCR and Chennai. Starting August 1st, 2013 only CTS-2010 compliant cheques could be submitted for clearing. But on July 17th, 2013 the deadline was reset to December 31st, 2013.What is the Purpose of Cheque Truncation System

The Cheque Truncation System (CTS) was introduced to reduce the time taken to collect cheques and clear them, thereby, improving customer service. The system also reduces the scope of clearing related frauds, reduces reconciliation errors, reduces the cost of collection, and almost eliminates logistics related problems. Even though there are other products on offer, such as, the Real Time Gross Settlement (RTGS) and the National Electronic Fund Transfer (NEFT) to make payments, many people prefer using cheques, keeping this in mind, the Reserve Bank of India (RBI) decided to increase the efficiency of the cheque clearing system. The CTS is a more secure system than the exchange of physical documents which requires the document to move from one point to another, ‘causing an increase in the processing time of cheques and there is a risk of the documents getting misplaced during transit, mutilated during transit or manipulated during transit.

What are the Charges?

The Reserve Bank of India has deregulated the charges to be levied by sponsor banks from user institutions. The sponsor banks are, however, required to disclose the charges in a transparent manner.Benefits To Beneficiary Customer

- The beneficiary need not visit his bank for depositing the paper instruments, which he would have otherwise received had he not opted for ECS Credit.

- The beneficiary need not be apprehensive of loss/theft of physical instruments or the likelihood of fraudulent encashment thereof.

- Cost effective.

- Benefits to Institution/ Govt. deptt. /Corporate clients beneficiary etc (User Clients)

- Savings on administrative machinery for printing, dispatch and reconciliation of paper instruments that would have been used had beneficiaries not opted for ECS Credit.

- Avoid chances of loss/theft of instruments in transit, likelihood of fraudulent encashment of paper instruments, etc.

- Efficient payment mode ensuring that the beneficiaries` get credit on a designated date. Cost effective.

There are two variants of ECS - ECS Credit and ECS Debit

ECS Credit

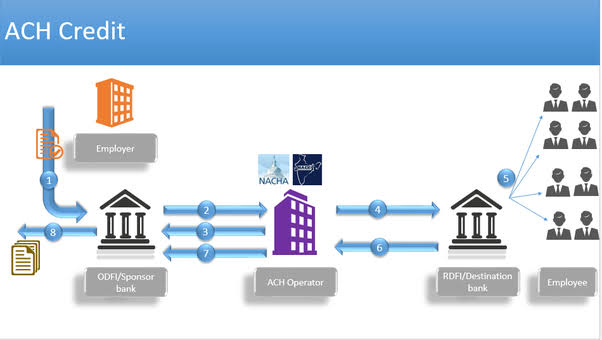

This is used by the institution for affording credit to a large number of beneficiaries (for instance, employees, investors etc.) having accounts with bank branches at various locations by raising a single debit to the bank account of the user institution. ECS Credit enables payment of amounts towards the distribution of dividend, interest, salary, pension, etc., of the user institution.ECS Debit

ECS Debit is used by an institution for raising debits to a large number of accounts (for instance, consumers of utility services, borrowers, investors in mutual funds etc.) maintained with bank branches at various locations for single credit to the bank account of the user institution. ECS Debit is useful for payment of telephone/electricity/water bills, cess/tax collections, loan installment repayments, periodic investments in mutual funds, insurance premium etc., that are periodic or repetitive in nature and payable to the user institution by a large number of customers etc.ECS scheme is distributed based on the geographical location of branches as:

- Local ECS – this is operating at 81 centres / locations across the country generally covering one city and/or satellite towns and suburbs adjoining the city.

- Regional ECS – this is operating at 9 centres / locations at various parts of the country and covers a State or group of States and can be used by institutions desirous of reaching beneficiaries within the State / group of States.

- National ECS – this is the centralized version of ECS Credit which was launched in October 2008. The Scheme is operated at Mumbai and facilitates the coverage of all core-banking enabled branches located anywhere in the country.

Locations where ECS managed by Reserve Bank of India

- Ahmedabad (Gujarat)

- Bengaluru (Karnataka)

- Bhubaneswar (Orissa)

- 4.Kolkata (West Bengal)

- Chandigarh (Punjab)

- Chennai (Tamil Nadu)

- Guwahati (Assam)

- Hyderabad (Andhra Pradesh)

- Jaipur (Rajsthan)

- Kanpur (Uttar Pradesh)

- 11.Mumbai (Maharashtra)

- Nagpur (Mahrashtra)

- New Delhi

- Patna (Bihar)

- Thiruvananthapuram (Kerala)

Comments

Post a Comment